This is an excellent article from Elena Popina at Bloomberg from the end of December 2018 explaining how recent stock market volatility is perfectly normal and has happened many, many times in the past:

The 2018 casualty list in markets is long. Hedge funds, Apple and Amazon’s trillion-dollar price tags, trading results everywhere. Not even Christmas was spared the wrath of cascading stocks. It has felt unprecedented, like Armageddon, or maybe even the robot apocalypse. It wasn’t.

While any 20 percent sell-off hurts, the one happening now is far from unheard of in terms of depth or velocity. Over the past 100 years, there are almost too many examples to count of stocks tumbling with comparable force.

“It’s an inevitable process,” Marshall Front, founder of Front Barnett Advisers, who began on Wall Street in 1963. “It goes on over and over again.”

Investors have time to reflect on history, now that stocks have avoided a fourth straight down week via the biggest one-day rally since 2009. After coming within a few points of a bear market on Wednesday, the damage in the S&P 500 stands at 15 percent since Sept. 20.

“This is very normal. It unnerves people because we’re all talking about it all the time,” said Nancy Tengler, chief investment strategist at Tengler Wealth Management. “It’s in our face more. We have too much focus on the day-to-day or minute-by-minute or second-by-second movements. Historically, is this normal? Yes.”

A fair amount of complaining has gone on in recent months about the role of high-frequency traders and quantitative funds in the drubbing that reached its peak around Christmas. Perhaps. Those groups are big, and in the search for villains, they make easy targets. Treasury Secretary Steven Mnuchin is among the people who have made the connection.

One thing that makes it tough to lay blame for the meltdown on machine-based traders is the many past instances when markets fell just as hard without their help. The Crash of 1929 is one big example. However bad this market is, it’s a walk in the park compared with then.

“The largest percentage changes, except for 1987, were in the ’20s and ’30s,” said Donald Selkin, chief market strategist at Newbridge Securities Corp. “You had dramatic moves then and you didn’t have electronic trading then.”

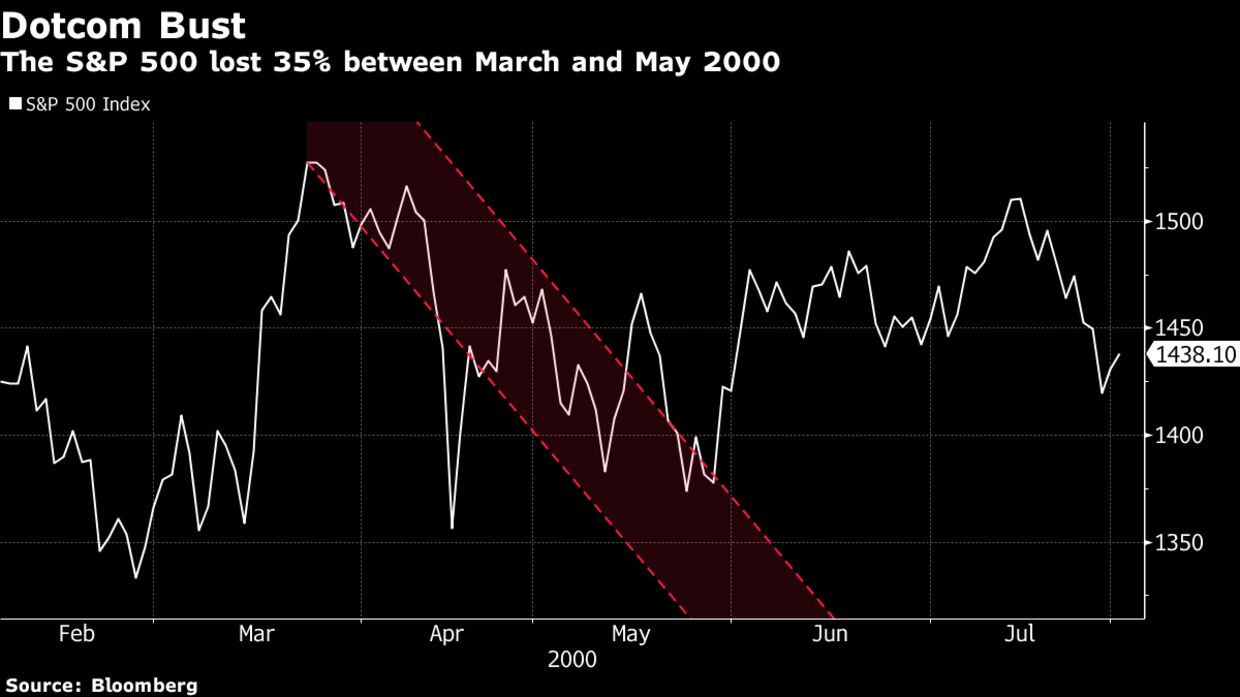

Dot-com Bust

The dot-com bubble that had been developing since the late 1990s popped in March 2000, when the S&P 500 lost 35 percent over the course of two months. It took the Nasdaq Composite Index, which peaked at 5,040.62 on March 10, about 15 years to get to its old high.

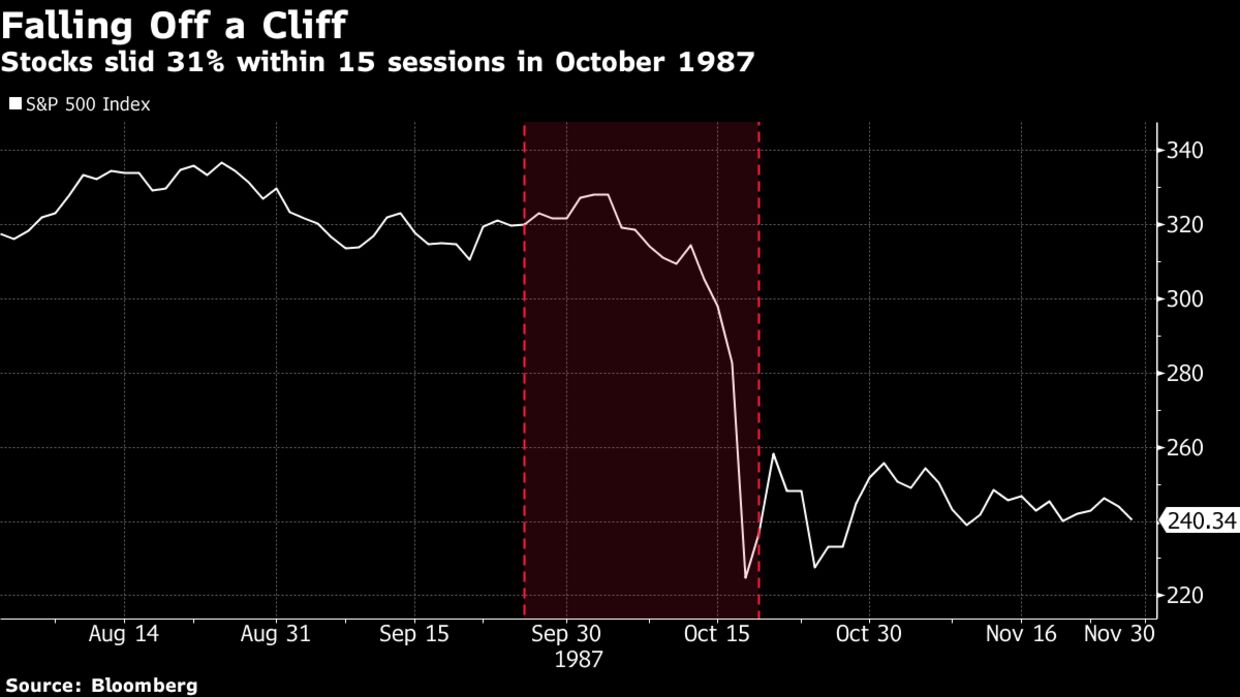

Black Monday of 1987

The S&P 500 rose 36 percent between January and August 1987 in what was set to be the best year in almost three decades. Then the October sell-off pushed the S&P into a 31 percent correction over just 15 days, much of it occurring in that one infamous session.

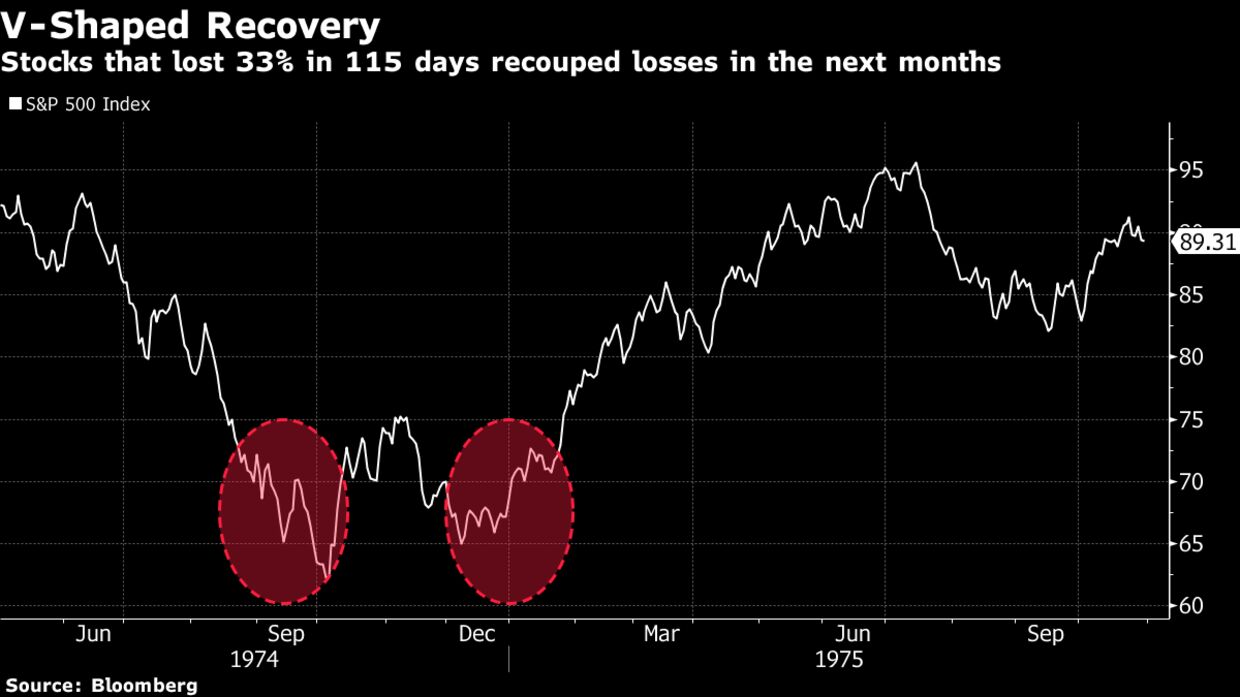

1974 Sell-Off

The worst year since 1937 for the S&P 500 saw the index fall 33 percent in 115 days as a weakening economy, rising unemployment and spiking inflation pushed investors to head for the exits. Stocks subsequently rebounded, surging more than 50 percent between October 1974 and July 1975.

1962 Rout

Investors of a certain age may recall 1962, when the S&P 500 Index lost a quarter of its value between March and June 1962. The rout known as the Kennedy Slide came after the S&P 500 advanced 79 percent in the prior four years. The S&P 500 was essentially flat over the next two decades.

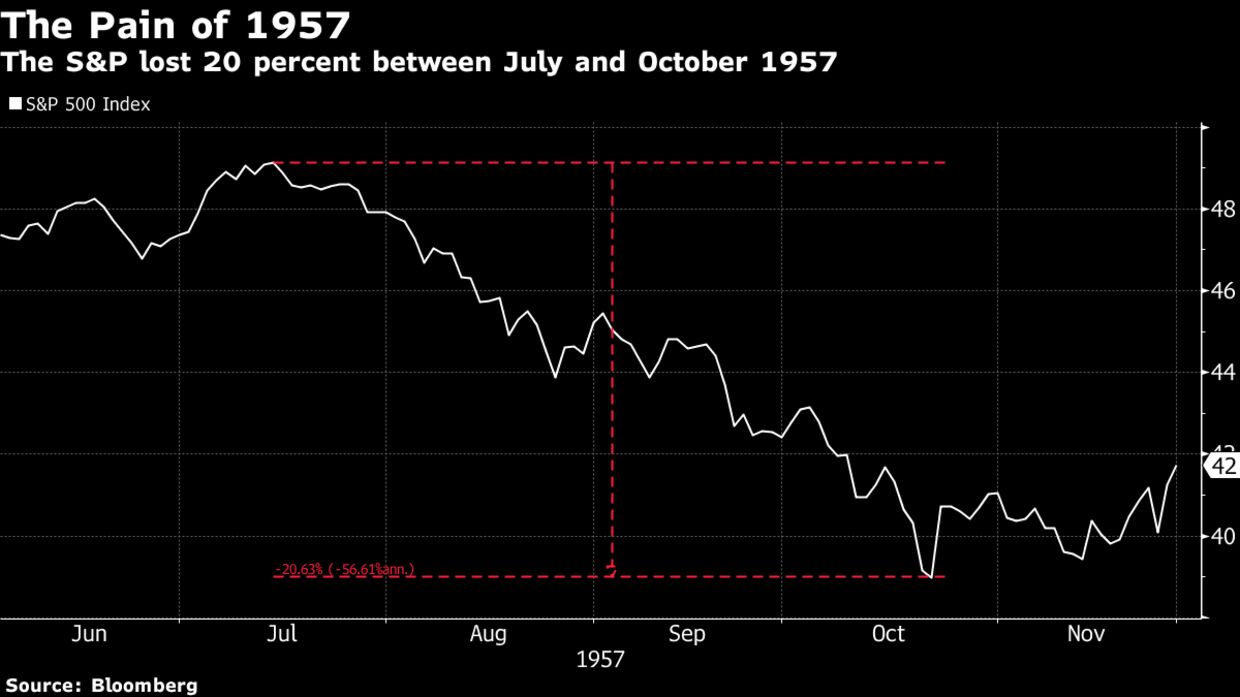

Not So Fat ’57

A dive in car sales and slowing housing construction pushed stocks into a 20 percent correction over 99 days in 1957. This preceded a recession that saw the U.S. gross domestic product contract 10 percent in a matter of three months in 1958.